Insights

I've got valuable information and resources to share. Explore away! And check back often.

First responders face financial challenges that are very different from most professions. Many retire earlier than traditional workers, often in their mid-50s, while Medicare doesn’t begin until 65. At the same time, they navigate physically demanding careers, higher stress levels, and an increased likelihood of medical expenses later in life. This creates real planning questions: • How do you bridge the health-care gap before Medicare? • How do pensions, Social Security, and personal savings work together? • How do you build income that lasts through a long retirement? These realities reinforce an important truth: retirement planning is not one-size-fits-all. Thoughtful, personalized planning can help turn complexity into clarity and replace uncertainty with confidence—especially for those who dedicate their careers to serving others. 📌 No products will be sold. See thrivent.com/social for important disclosures.

First responders face financial challenges that are very different from most professions. Many retire earlier than traditional workers, often in their mid-50s, while Medicare doesn’t begin until 65. At the same time, they navigate physically demanding careers, higher stress levels, and an increased likelihood of medical expenses later in life. This creates real planning questions: • How do you bridge the health-care gap before Medicare? • How do pensions, Social Security, and personal savings work together? • How do you build income that lasts through a long retirement? These realities reinforce an important truth: retirement planning is not one-size-fits-all. Thoughtful, personalized planning can help turn complexity into clarity and replace uncertainty with confidence—especially for those who dedicate their careers to serving others. 📌 No products will be sold. See thrivent.com/social for important disclosures.

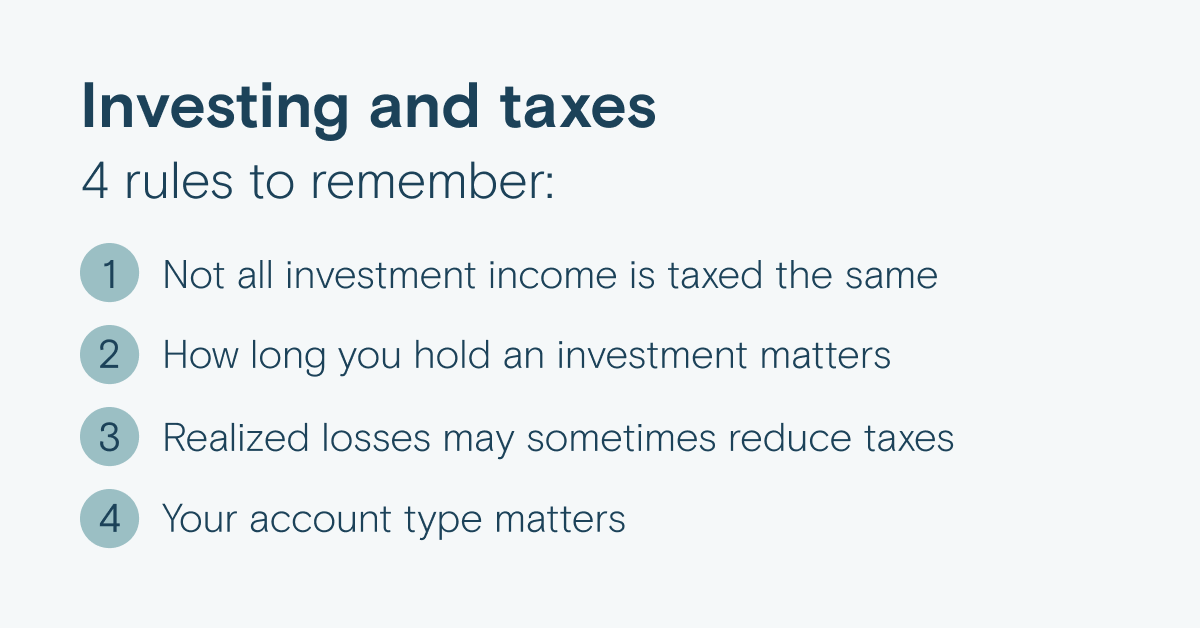

If you’re relatively new to investing, understanding the basics of how realized gains and losses are taxed can help you make smarter decisions. These 4 rules are a great place to start. 📌 For more, check out this guide: https://bit.ly/4p4h9Hn

If you’re relatively new to investing, understanding the basics of how realized gains and losses are taxed can help you make smarter decisions. These 4 rules are a great place to start. 📌 For more, check out this guide: https://bit.ly/4p4h9Hn

Key Financial Factors First Responders Should Review in 2025 Many first responders are reevaluating their financial plans this year. Here are a few areas worth paying attention to: Overtime fluctuations: Variable income can affect long-term savings projections and retirement planning. Retirement plan updates: Some agencies are adjusting contribution limits or pension guidelines—knowing your plan’s details is essential. Cost-of-living increases: Rising expenses make regular cash-flow checkups more important. 401(a) and 457(b) strategies: Understanding contribution rules, distribution timing, and tax considerations helps you use these plans effectively. Earlier retirement timelines: Many first responders retire sooner than other professions, so reviewing benefits, healthcare options, and income sources is important. I focus on providing educational guidance tailored to first responders, helping you understand how these factors may influence your long-term financial planning. 📌 No products will be sold. See thrivent.com/social for important disclosures.

Key Financial Factors First Responders Should Review in 2025 Many first responders are reevaluating their financial plans this year. Here are a few areas worth paying attention to: Overtime fluctuations: Variable income can affect long-term savings projections and retirement planning. Retirement plan updates: Some agencies are adjusting contribution limits or pension guidelines—knowing your plan’s details is essential. Cost-of-living increases: Rising expenses make regular cash-flow checkups more important. 401(a) and 457(b) strategies: Understanding contribution rules, distribution timing, and tax considerations helps you use these plans effectively. Earlier retirement timelines: Many first responders retire sooner than other professions, so reviewing benefits, healthcare options, and income sources is important. I focus on providing educational guidance tailored to first responders, helping you understand how these factors may influence your long-term financial planning. 📌 No products will be sold. See thrivent.com/social for important disclosures.

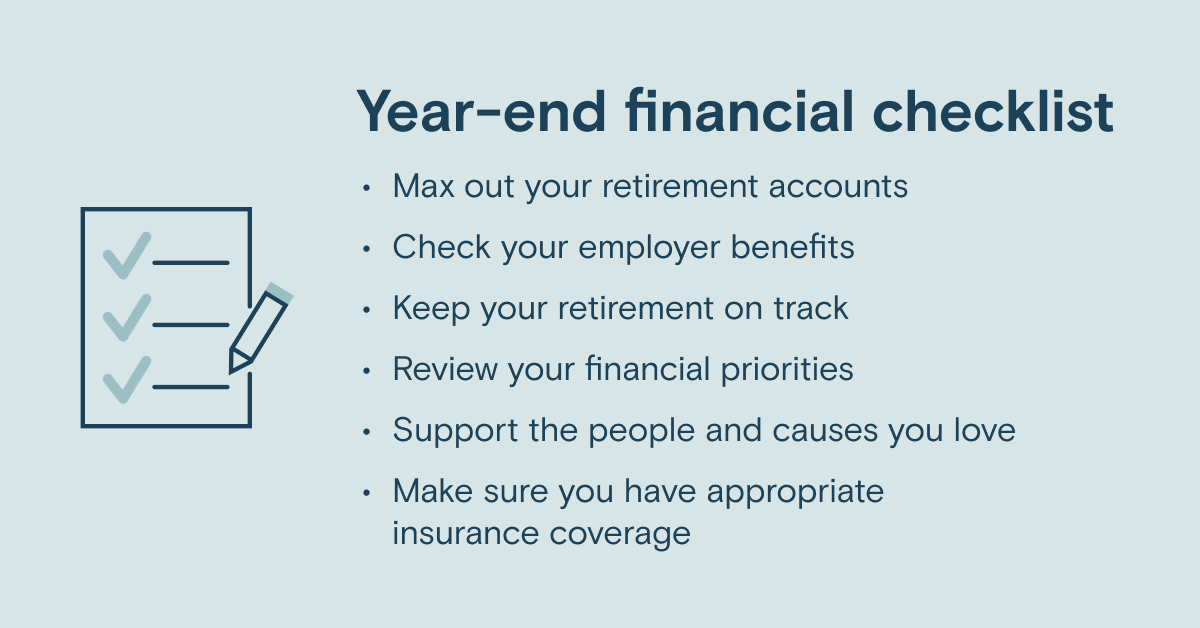

It’s hard to believe the year is already winding down! While shopping, baking and holiday gatherings may be at the top of your to-do list, don’t forget to carve out time for a year-end financial checkup. Taking these 6 steps now can help you minimize your taxes, strengthen your savings and start the new year on solid footing. 👉 If you’d like personalized guidance, let’s connect. See thrivent.com/social for important disclosures. Thrivent and its financial advisors and professionals do not provide legal, accounting or tax advice. Consult your attorney or tax professional.

It’s hard to believe the year is already winding down! While shopping, baking and holiday gatherings may be at the top of your to-do list, don’t forget to carve out time for a year-end financial checkup. Taking these 6 steps now can help you minimize your taxes, strengthen your savings and start the new year on solid footing. 👉 If you’d like personalized guidance, let’s connect. See thrivent.com/social for important disclosures. Thrivent and its financial advisors and professionals do not provide legal, accounting or tax advice. Consult your attorney or tax professional.

🚓 First Responders: Are You Maximizing Your Year-End Benefits? 🚒 Before the calendar flips, now is the perfect time to review financial tools and benefits designed to support you and your family. Some key areas to check: • Retirement Accounts: Review your contributions to your 401(a), 457, or IRAs. • Tax Deductions: Don’t miss work-related expenses, charitable contributions, or other eligible deductions. • Health Savings Accounts: Eligible HSAs can provide tax-advantaged growth for medical expenses. • Education & Professional Development: Use any remaining allowances for certifications, licenses, or training. • Emergency & Education Savings: Extra income or seasonal pay can be directed to savings or 529 plans. • Insurance Review: Confirm health, life, and long-term care coverage is current. • Work-Related Benefits: Make sure all allowances, stipends, or perks are used before year-end. 🔎 A structured year-end review can ensure benefits are fully utilized and financial records are organized for the year ahead. 📌 No products will be sold. See thrivent.com/social for important disclosures.

🚓 First Responders: Are You Maximizing Your Year-End Benefits? 🚒 Before the calendar flips, now is the perfect time to review financial tools and benefits designed to support you and your family. Some key areas to check: • Retirement Accounts: Review your contributions to your 401(a), 457, or IRAs. • Tax Deductions: Don’t miss work-related expenses, charitable contributions, or other eligible deductions. • Health Savings Accounts: Eligible HSAs can provide tax-advantaged growth for medical expenses. • Education & Professional Development: Use any remaining allowances for certifications, licenses, or training. • Emergency & Education Savings: Extra income or seasonal pay can be directed to savings or 529 plans. • Insurance Review: Confirm health, life, and long-term care coverage is current. • Work-Related Benefits: Make sure all allowances, stipends, or perks are used before year-end. 🔎 A structured year-end review can ensure benefits are fully utilized and financial records are organized for the year ahead. 📌 No products will be sold. See thrivent.com/social for important disclosures.

Taxes can quietly shrink your retirement savings. Even small changes in what you pay can make a big difference. Reach out to discuss ways to keep more of what you’ve earned. See thrivent.com/social for important disclosures.

Taxes can quietly shrink your retirement savings. Even small changes in what you pay can make a big difference. Reach out to discuss ways to keep more of what you’ve earned. See thrivent.com/social for important disclosures.

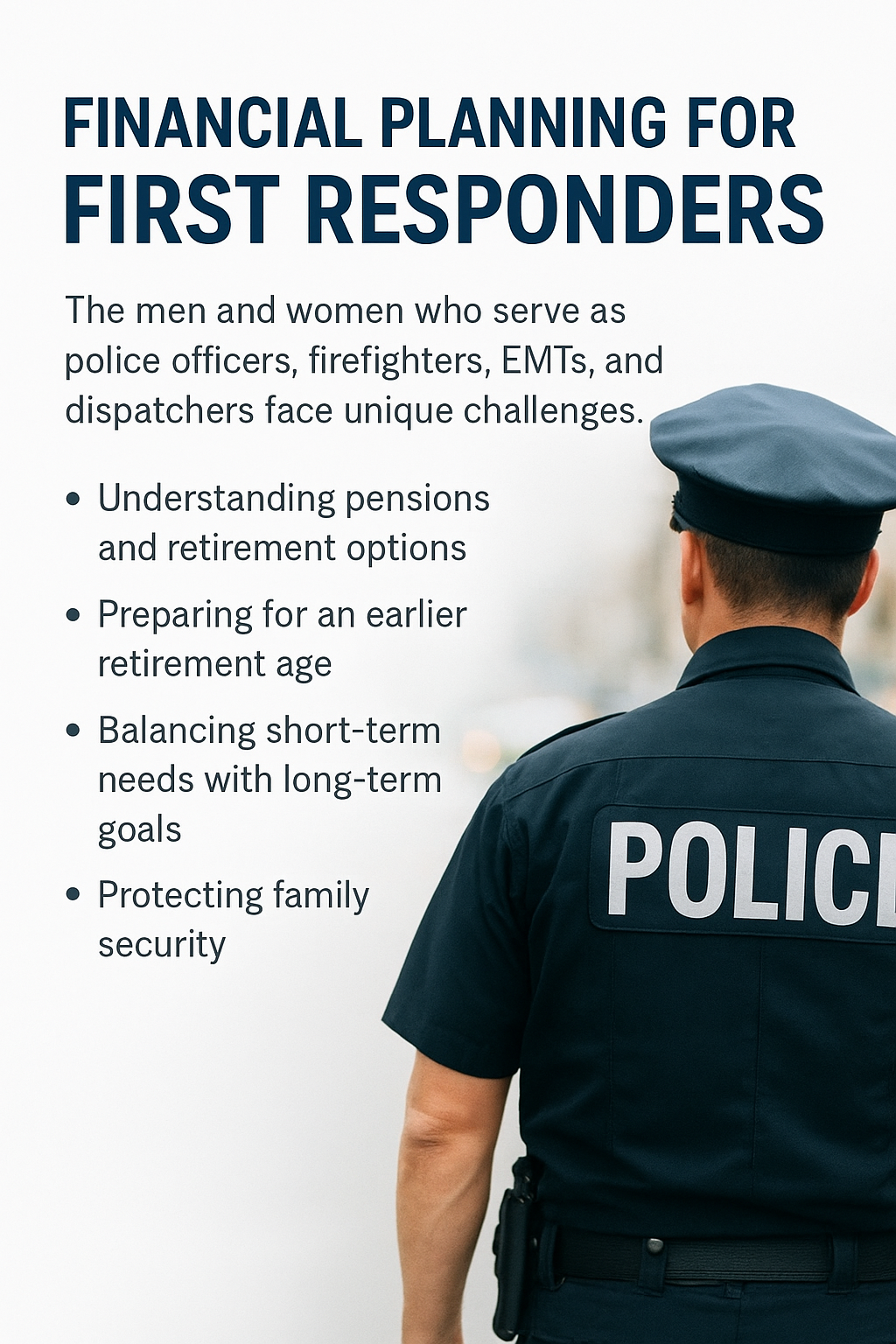

Financial Planning for First Responders The men and women who serve as police officers, firefighters, EMTs, and dispatchers face unique challenges. The demands of long shifts, physical risks, and the mental toll of the job often leave little time to focus on personal financial health. Yet, having a plan in place can make a real difference. For many first responders, financial planning may involve: Understanding pensions and retirement options – such as 401(a), 457(b), and DROP programs, which each have unique rules. Preparing for an earlier retirement age – common in this field, but requiring careful planning to ensure assets last. Balancing short-term needs with long-term goals – like paying down debt, saving for children’s education, or creating a retirement income strategy. Protecting family security –prepare for the unexpected, both on and off the job. Addressing health and wellness – recognizing that financial stress is closely tied to overall well-being. As a former police officer, I’ve seen firsthand the sacrifices first responders and their families make. Today, my focus is helping them understand their options, so they can have a better understanding of the future they’re working so hard to protect. If you’re a first responder — or support someone who is — I’m always happy to share educational resources and start a conversation about the unique financial factors in this profession. 📌 No products will be sold. See thrivent.com/social for important disclosures.

Financial Planning for First Responders The men and women who serve as police officers, firefighters, EMTs, and dispatchers face unique challenges. The demands of long shifts, physical risks, and the mental toll of the job often leave little time to focus on personal financial health. Yet, having a plan in place can make a real difference. For many first responders, financial planning may involve: Understanding pensions and retirement options – such as 401(a), 457(b), and DROP programs, which each have unique rules. Preparing for an earlier retirement age – common in this field, but requiring careful planning to ensure assets last. Balancing short-term needs with long-term goals – like paying down debt, saving for children’s education, or creating a retirement income strategy. Protecting family security –prepare for the unexpected, both on and off the job. Addressing health and wellness – recognizing that financial stress is closely tied to overall well-being. As a former police officer, I’ve seen firsthand the sacrifices first responders and their families make. Today, my focus is helping them understand their options, so they can have a better understanding of the future they’re working so hard to protect. If you’re a first responder — or support someone who is — I’m always happy to share educational resources and start a conversation about the unique financial factors in this profession. 📌 No products will be sold. See thrivent.com/social for important disclosures.